AI For Trading: SMB 和 HML (55)

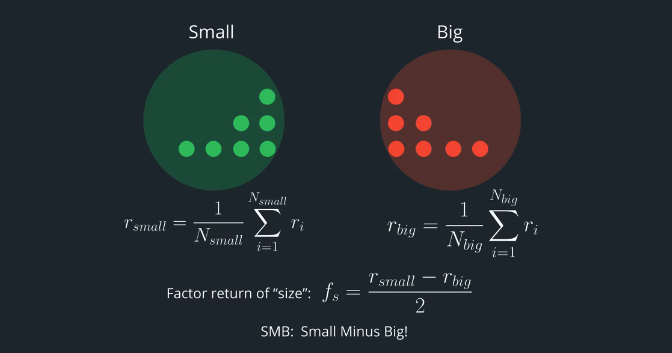

SMB

To create a theoretical portfolio representing size, we could go long the bottom 10th percentile of stocks by market cap (long small cap stocks) and go short stocks above the 90th percentile (go short the large cap stocks). We could assume an equal dollar amount invested in each stock. In the above example, we are dividing by 2 to take the average return of going long small cap stocks and going short large cap stocks.

为了创建一个代表规模的理论投资组合,我们可以通过市值(长期小盘股)走多头股票的底部10个百分点,并且做空股票超过90个百分点(做空大盘股)。我们可以假设每股股票投入相同的美元金额。在上面的例子中,我们除以2来得出长期小盘股和短期大盘股的平均回报率。

It's also common to compute the spread between two portfolios. One portfolio contains the small cap stocks, and the other portfolio contains the large cap stocks. In this case, we'd just take the difference between the returns of the two portfolios.

计算两个投资组合之间的差价也很常见。一个投资组合包含小盘股,另一个投资组合包含大盘股。在这种情况下,我们只是考虑两个投资组合的回报之间的差异。

SMB = Small minus Big

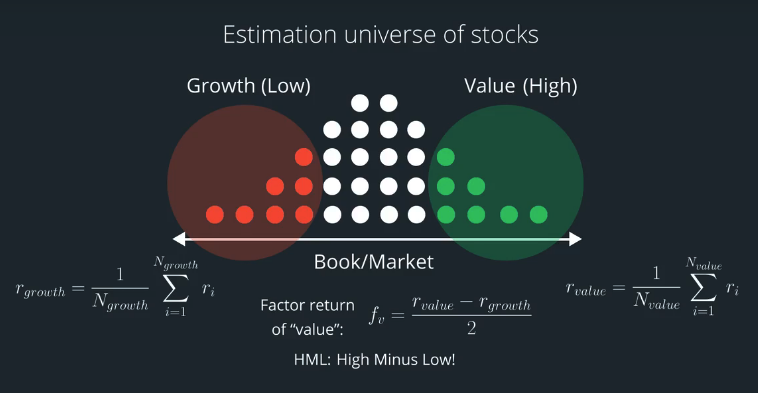

HML

HML = High minus Low

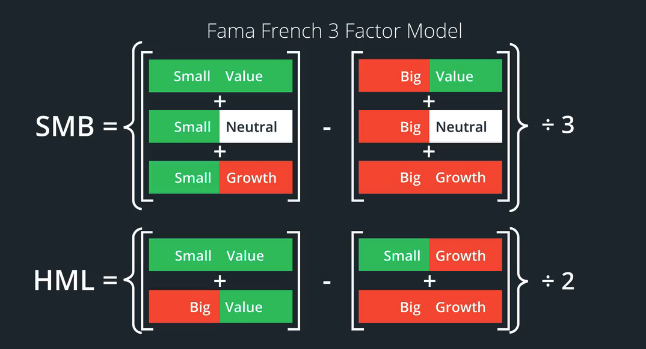

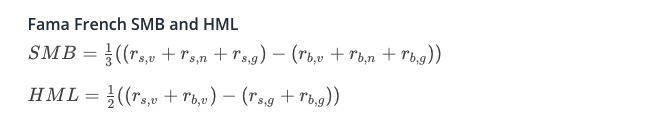

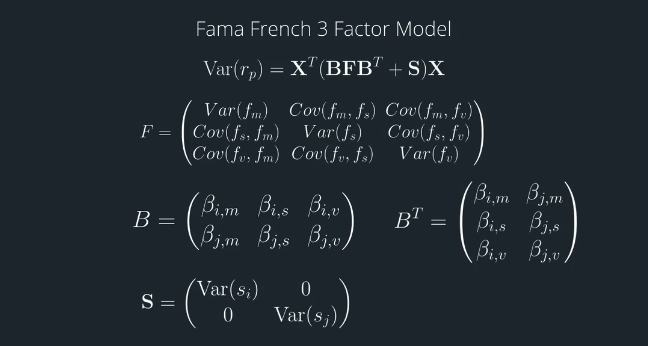

Fama French SMB and HML

Fama French Risk Model

Matrix of Factor Returns

Calculate the covariance matrix using the time series of factor returns.

Matrix of Factor Exposures

Use a multiple regression to estimate the factor exposures.

Specific Variance

Calculate the actual minus estimated returns as the specific return. The variance of that time series is an estimate of specific variance.

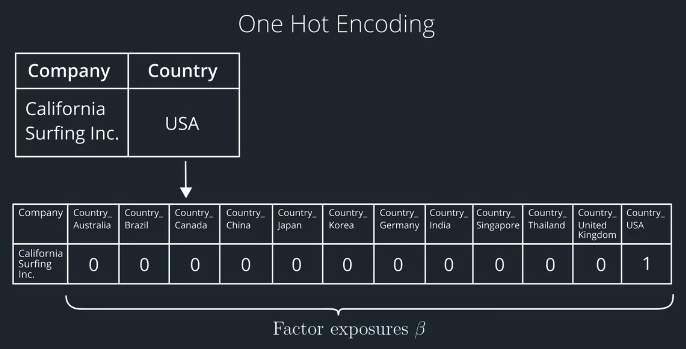

Categorical Factors

When handling categorical variables, we can make each unique value within a category be its own variable. In this example, the country variable becomes "country_usa", "country_india", "country_brazil" etc. Then assign a value to each of these variables to represent how "exposed" the company is to each country.

Estimating Factor Return

If we collect a cross-section of multiple stocks for a single time period, then we'll have pairs of stock returns and factor exposures. We can use regression to estimate the factor return for that single time period. Then repeat over multiple time periods to get a time series of factor returns.

如果我们在一个时间段内收集多个股票的横截面,那么我们将有一对股票收益和因子风险。我们可以使用回归来估计该单个时间段的因子回报。然后重复多个时间段以获得因子返回的时间序列。

为者常成,行者常至

自由转载-非商用-非衍生-保持署名(创意共享3.0许可证)