AI For Trading:Alpha Factors Summary (74)

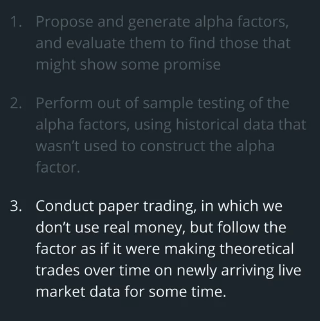

We first propose and generate alpha factors,then evaluate them to find those that might show some promise.

我们首先提出并生成alpha因子,然后对它们进行评估以找到那些可能显示出一定承诺的因子。

Then we perform out-of-sample testing of the alpha factors using historical data that wasn't used to construct the alpha vector.

然后,我们使用未用于构建alpha矢量的历史数据对alpha因子进行样本外测试。

If that looks promising,then we would conduct paper trading in which we don't use real money,but we follow the factor as if we're making theoretical trays over time on newly arriving live market data for some period.

如果这看起来很有希望,那么我们将进行纸质交易,其中我们不使用真钱,但我们遵循这个因素,好像我们在一段时间内对新到的实时市场数据进行理论托盘。

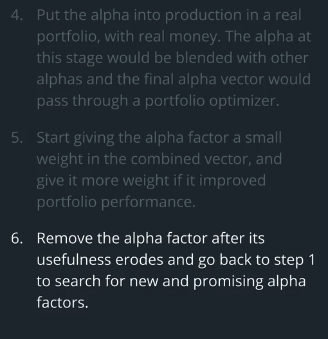

If that showed promise,then we would put the alpha into production in a real portfolio with real money.The alpha at that stage would be blended with other alphas and the final alpha vector would pass through a portfolio optimizer.

如果这显示出了希望,那么我们就会将alpha投入到真实投资组合的生产中。该阶段的alpha将与其他alpha混合,最终的alpha矢量将通过投资组合优化器。

We would likely start by giving that alpha factor a small weight in the combined vector, and given more weight if it performed and improved portfolio performance.

我们可能首先在组合向量中给予α因子一个小的权重,并且如果它执行并提高了投资组合的性能,则给予更多的权重。

We would monitor the alpha factor over time knowing that at some point, the factor's usefulness will erode because we're trading in a competitive market. Then, we would remove the alpha factor and go back to the beginning to search for new promising alpha factors.

我们会随着时间的推移监控α因子,因为我们知道在某些时候因为我们在竞争激烈的市场中交易,因此该因素的有用性将会受到侵蚀。然后,我们将删除alpha因子并回到开头搜索新的有希望的alpha因子。

为者常成,行者常至

自由转载-非商用-非衍生-保持署名(创意共享3.0许可证)